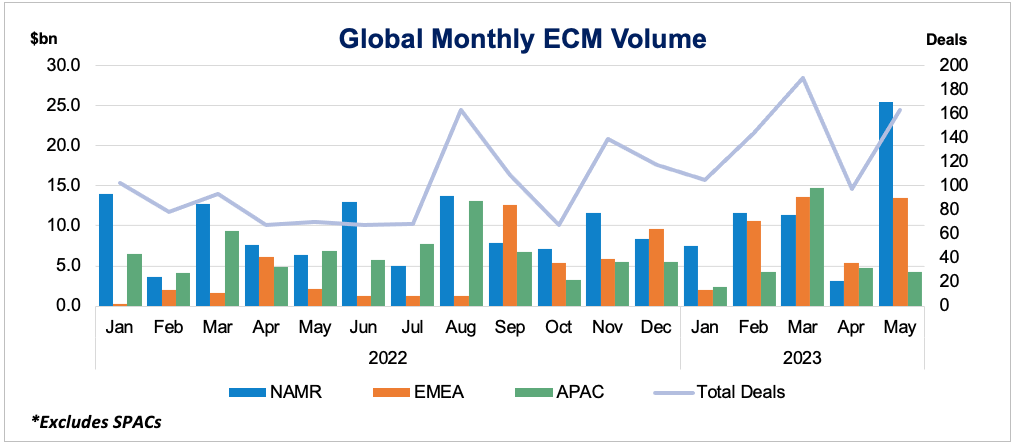

Global ECM activity rebounded in May with 163 offerings raising a combined $41.8bn, according to CMG data. This followed a sluggish April which produced a modest $13.8bn via 100 transactions, the lowest monthly deal count since October 2022. The US and Canada jointly led the way with a combined 91 offerings amounting to $25.4bn.

CMG data illustrates that the $5.6bn raised via US IPOs in May surpasses the combined total of the preceding four months of US IPO activity. Overall US ECM activity has rebounded as well, with $25.1bn raised in May compared to the $3.1bn tally in April. As the US IPO market continues to gain momentum, the EMEA IPO market remains stable, supported by CMG data that shows a monthly decrease of only 5% from April ($906mm) to May ($860mm). The Middle East continues to be the leading region within EMEA with all 5 IPOs listed in either Saudi Arabia or UAE.

The $3.8bn Kenvue Inc. IPO on May 3 may have opened the door to more activity as the largest US IPO since the debut of Rivian Automotive on November 9, 2021. Looking ahead, momentum continues as the CMG Global calendar reflects 3 follow-ons pricing in the first week of June worth over $1bn each: Corebridge Financial, GE Healthcare, and Mobileye Global. The market’s attention remains focused on the Fed’s actions and the latest economic data, which will likely impact whether the volume of deals will continue to increase.