TL;DR

- Global equity issuance rebounded in January, with the U.S., EMEA and APAC all posting year-over-year growth in capital raised.

- U.S. activity accelerated, driven by follow-on offerings and the strongest month for SPAC issuance since 2021.

- Industrials led sector issuance, topping capital raised in both the U.S. and EMEA and delivering strong dollar-weighted aftermarket performance.

- APAC dominated by deal count, while EMEA issuance was supported by large-cap transactions and improving investor risk appetite.

U.S. Equity Issuance Activity Accelerates

U.S. equity issuance showed a notable pickup in January, with 40 offerings raising $14.0B, representing a 43% increase year-over-year. The rebound in capital raised suggests improving issuer confidence and growing investor appetite, particularly for the 33 follow-on offerings, which accounted for a significant share of activity.

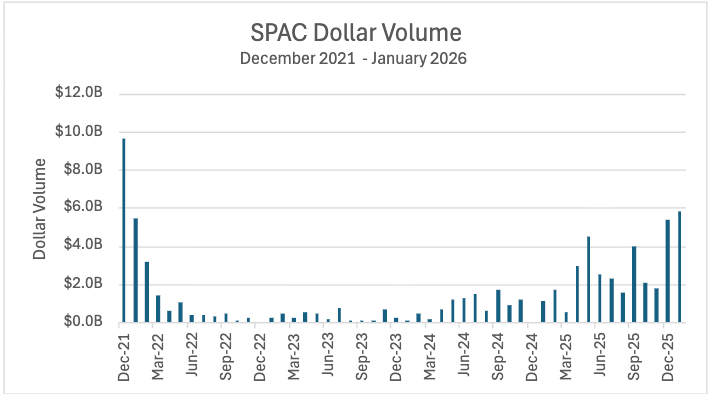

Hottest Month for U.S. SPACs Since 2021

SPAC issuance posted $5.8B in capital, the strongest month in years, marking the most active period since December 2021 with $9.6B. While overall volumes remain well below peak-cycle levels, the sharp inflection signals a thawing in a segment that has been largely dormant.

Industrials Take the Lead

After several months of healthcare-led issuance ($4.5B raised in the U.S. and no activity in EMEA), Industrials emerged as a standout sector, leading capital raised with $5.1B in the U.S. and $5.6B in EMEA.

Performance has been strong, with EMEA Industrials delivering a +26.5% dollar-weighted average return on day 1, while U.S. Industrials posted +6.0%. This strength mirrors the outperformance explored in Markets Cool in October. Dutch industrials company CSG B.V.’s (CSG) $4.5B IPO included an overallotment that was fully exercised and delivered a 31.4% first-day gain, underscoring strong investor demand for high-quality industrial issuers.

EMEA and APAC Drive the Story

Outside the U.S., issuance activity was led by EMEA and APAC, both posting meaningful year-over-year growth in capital raised. EMEA issuance totaled $7.2B across 11 offerings, driven by large-cap Industrials and financials amid improving macro conditions. APAC raised $11.2B across 44 offerings, leading globally by deal count.

January’s issuance data points to a broadening recovery in global ECM activity, marked by increased U.S. follow-ons, a SPAC revival, sector rotation toward Industrials and strengthening pipelines in EMEA and APAC. If trends continue, Industrials may remain a focal point for issuance and aftermarket outperformance in the months ahead.