TL;DR

- U.S. activity driven by strength in Technology, as the sector led overall proceeds through follow-ons, convertibles, and significant ATM program announcements.

- Energy issuance in North America was defined by secondary liquidity, with 100% secondary transactions representing the majority of proceeds as sponsors monetized into strong sector performance.

- SPAC issuance sustained momentum with $5B+ raised for the third consecutive month.

- Global issuance remained active led by North America with $25B+ raised across the U.S. and Canada, while APAC and EMEA delivered steady but comparatively lower volumes. APAC demonstrated robust investor demand, particularly in Technology, which delivered a +30.85% average 1-day return.

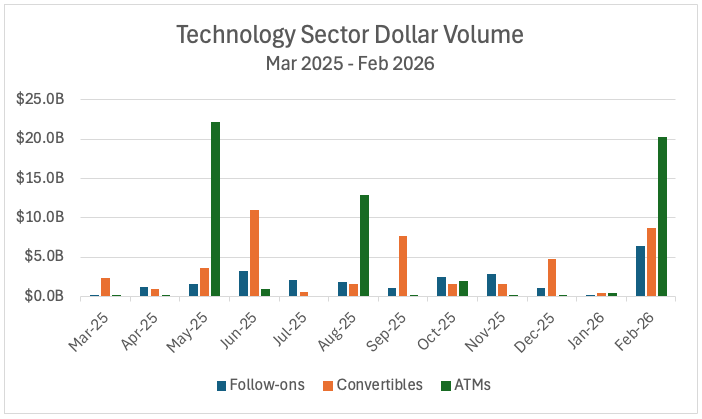

U.S. Technology Led Proceeds

Technology led all sectors in U.S. proceeds, across traditional follow-on offerings, convertibles and ATM (at-the-market) program filings.

- $6.4B – Follow-Ons

- $8.7B – Convertible offerings

- $20.3B – ATM programs announced across 3 issuers

Of issuers coming to market in February, Oracle Corporation (ORCL) took the spotlight with their $5B convertible offering and $20B ATM announcement. Oracle stock most notably fell ~(10.88)% following three days from the ATM filing data and bond close.

Track Oracle and other ATM selldown activity with CMG, contact us to learn more.

N. America Energy: Strong Performance Meets Secondary Liquidity

100% secondary proceeds were a defining theme for the energy sector in North America. Holistically, the sector saw 10 offerings across Canada and the U.S. that raised $2.5B, seven of which were structured with 100% secondary shares that contributed to $1.9B of issuance for the month of February.

Notable secondary liquidity included:

- Private equity firm Kimmeridge’s clean-up trade of SM Energy (SM)

- Abu Dhabi Investment Authority’s large sell-down of 10,377,954 shares of Vista Energy (VIST)

- Brookfield Asset Management’s 15,260,000 shares of Rockpoint Gas Storage (RGSI)

The prevalence of fully secondary transactions suggests sponsors and insiders are capitalizing on strong sector valuations. Supporting this backdrop, the State Street Energy Select Sector SPDR ETF (XLE) reflected a +26% returns YTD, reinforcing favorable market conditions for monetization activity within the energy sector.

SPAC Momentum Holds with a Third Straight $5B+ Month

SPAC IPO activity, which began accelerating in 2024 and gained momentum through 2025 as mentioned in prior market insight pieces, continued its upward trajectory in February. SPAC proceeds exceeded $5B for the third consecutive month.

This sustained capital formation signals renewed institutional comfort with the SPAC structure following the lull in activity post 2021.

Issuance Across Global Regions

North America

United States: 60 offerings | $23.7B raised

The U.S. remained the dominant issuance hub in February, supported by strength in Technology, Energy, and Basic Materials.

Canada: 6 offerings | $1.5B raised

Historically, Canadian ECM activity has frequently trended below $1B in monthly issuance over recent years. February’s $1.5B total places financing activity well above long-term country averages, signaling a meaningful rebound in larger-ticket equity raises.

Asia-Pacific

APAC: 44 offerings | $13.9B raised

APAC issuance remained active, with the Technology sector driving outsized performance. Notably, the sector delivered a +30.85% average 1-day return, highlighting strong investor demand and pricing power for growth-oriented issuers.

Europe, the Middle East and Africa

EMEA issuance remained constructive, though volumes trailed against North America and APAC. Activity was steady but more concentrated relative to prior months.

Latin America

LatAm: 1 offering | $583.6M raised

Latin America saw limited activity in February, with a single offering.